and keep all the other monetary accommodations.

Zero Hedge has the article that contains detailed analysis, but here's my summary:

Goldman Sachs' chief economist Jan Hatzius, who said the Fed could easily double the balance sheet to $4 trillion back in August 2009, now says $4 trillion addition to the existing balance sheet is needed to completely fill the gap between the official fed funds rate and the Taylor-implied fund rate, which is minus 7%.

I can almost see your eyes rolling... "What the @#$% is the Taylor-implied fund rate?" I will get to that shortly, but on with the GS economist's take...

Of that gap, Hatzius thinks 4% is already filled by 1) already near zero fed funds rate; 2) QE1; 3) communication from the Fed that it is committed to the near zero fed funds rate. That leaves 3% to fill.

Unlike the NY Fed president Dudley who said $500 billion QE2 would be equal to 0.75% rate reduction, Hatzius thinks it would take $1 trillion to achieve the effect of 0.75% rate reduction. Thus, it would take $4 trillion to fill the 3% gap.

The Federal Reserve would not do $4 trillion QE2, says Hatzius, as it fears the "tail risks" of expanding the balance sheet, one of which is "substantial mark-to-market investment losses".

Ding ding ding ding... Maybe the NY Fed is suing Countrywide/Bank of America seriously, and for a very good reason.

So his prediction is the same as in 2009, that the Fed will eventually expand the balance sheet by $2 trillion. The question is how soon the Fed will converge with Goldman's assessment, he says. (I wonder if it is a rhetorical question..)

Now, "the Taylor-implied fund rate". You think it is some kind of economist gibberish (it is, actually) but the gibberish is taken very seriously at the Fed in crafting its monetary policies. And so you should be aware in order to front-run the Fed to protect your wealth.

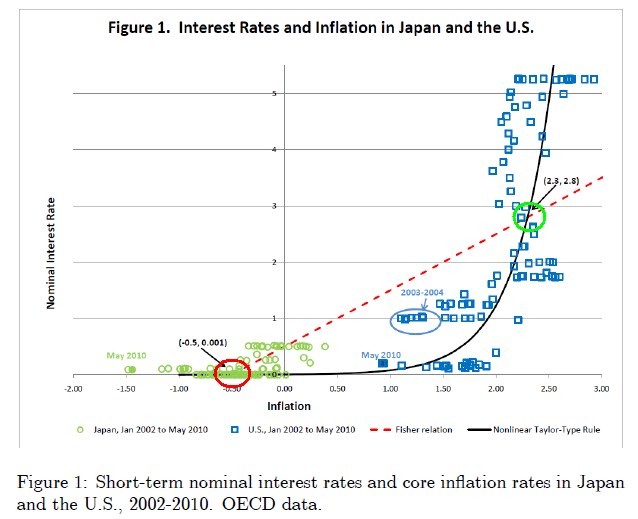

First, who or what is "Taylor"? Taylor is the name of an economist at Stanford University who proposed the Taylor rule. The Taylor curve is derived from the rule, and indicates how the central bank should change the nominal interest rate in response to a given price inflation rate, and it looks like this (the chart was taken from the paper written by James Bullard, St. Louis Fed president):

It's that curved line. The red dotted line intersecting the Taylor curve is called "the Fisher relation" (Nominal Interest Rate= Real interest Rate + Expected Inflation Rate), and the two sections that these two lines intersect are "stable" points to the Fed which I circled in green and red. The Fed wants the green circle, and Japan is seemingly stuck around the red circle for two decades.

Since the official fed funds rate cannot be set below 0%, the Taylor curve flattens at about 1% price inflation and 0.1% fed funds rate and remains flat all the way into price deflation.

The Taylor-implied fund rate is basically a rate if the fed funds rate were allowed to go negative at a given price inflation rate. Bullard's paper has a chart that shows the Taylor curve, or rather "line" in this case, going straight through zero, instead of flattening out at zero. Since Bullard's chart didn't go below -3% on the Y-axis (nominal interest rate), I added a few lines and extended the Taylor "line". Surprise, surprise. At a price inflation rate of 1% (that's what we are at, supposedly), the fed funds rate should be -7%!

So, how can the Fed effectively achieve a negative fed funds rate? That's where the quantitative easing comes.

As mentioned above, NY Fed's Dudley thinks $500 billion QE will achieve effective rate reduction of 0.75%, while Goldman's Hatzius thinks $1 trillion will do the trick. So, to fill 3% gap that remains, the Fed needs $4 trillion.

That is, if Hatzius is right in $1 trillion per 0.75%. If $1 trillion only achieves 0.5% reduction, the Fed would need $5 trillion newly printed money. It also depends on whether Hatzius' estimate is correct that 4% of the 7% gap has already been filled. What if the estimate is incorrect? What if ZIRP didn't contribute, and QE1 only achieved 1% gap-fill? The Fed would have 6% to fill, and that would take $8 trillion.

Got food? Got shelter? Got ammo? Got gold and silver?

As long as the numbers add up or line up neatly on the chart, these economists at the Fed or at Goldman Sachs do not quite care what may or may not happen on Main Street. QE1 was all about propping up TBTF banks and inviting insiders to benefit (PIMCO comes to mind, who dumped Treasuries and agency MBS on the Fed). QE2 should be no different. Excess reserves that banks hold at the Fed hasn't escaped much into Main Street. Banks don't lend, people and businesses don't borrow from the bank - either they can't, due to destroyed credit thanks to the TBTF banks, or they don't want to.

As a non-economist without PhD, I find it scary that PhD economists seem to take this "Taylor rule" and "Fisher relation" pretty much as given. They look to me like "hypothesis" at best. What if they are wrong? What if the Taylor "line" below 0% nominal interest rate is not as steep as the above-zero line? The Fed would end up pumping way more money into the system than warranted, possibly triggering a massive inflation and massive devaluation of US dollar.

I also quite don't understand the Fed officials' confidence in a gradual approach ($100 billion per month QE). The response may not be linear but chaotic (in a mathematical sense). After several weeks, months of steady QE2, prices may jump out of the blue or US dollar crash 10% in a day, and the Fed may not have any control. "Tail risks" are not just for the Fed balance sheet.

If and when things blow up beyond their control, I already know what the Fed officials' excuse will be: "Who could have known? We meant well..."

Tokyo Time

Tokyo Time

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)

{kind=link}

{kind=link}

0 comments:

Post a Comment